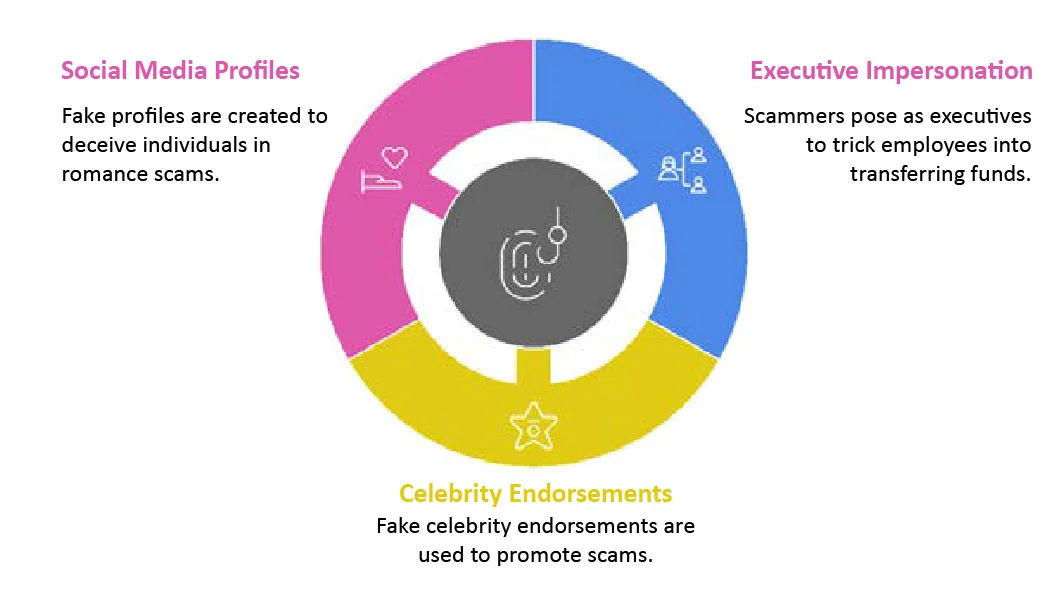

Deepfake Technology: Scammers are increasingly using deepfake technology to impersonate individuals, including family members or executives, to manipulate victims into transferring money or divulging sensitive information. This technology allows scammers to create convincing audio/videos of people saying or doing things they never actually did. Deepfakes are being used for various scams, such as:

Generative AI for Fake Content: Fraudsters can use AI to generate convincing fake texts, images, and videos, which can be employed to create fraudulent advertisements or impersonate individuals. This capability allows for the creation of synthetic identities that can evade Know Your Customer (KYC) protocols and facilitate account takeovers.

AI scams often target customers directly, bypassing established banking systems, which is a significant shift from traditional fraud management. But now as customers have become ‘digital natives’, it is easier for them to reach out to customers directly. In fact, many a time, the fraudsters pose as employees of the bank! This shift poses significant challenges for financial institutions and risk leaders.

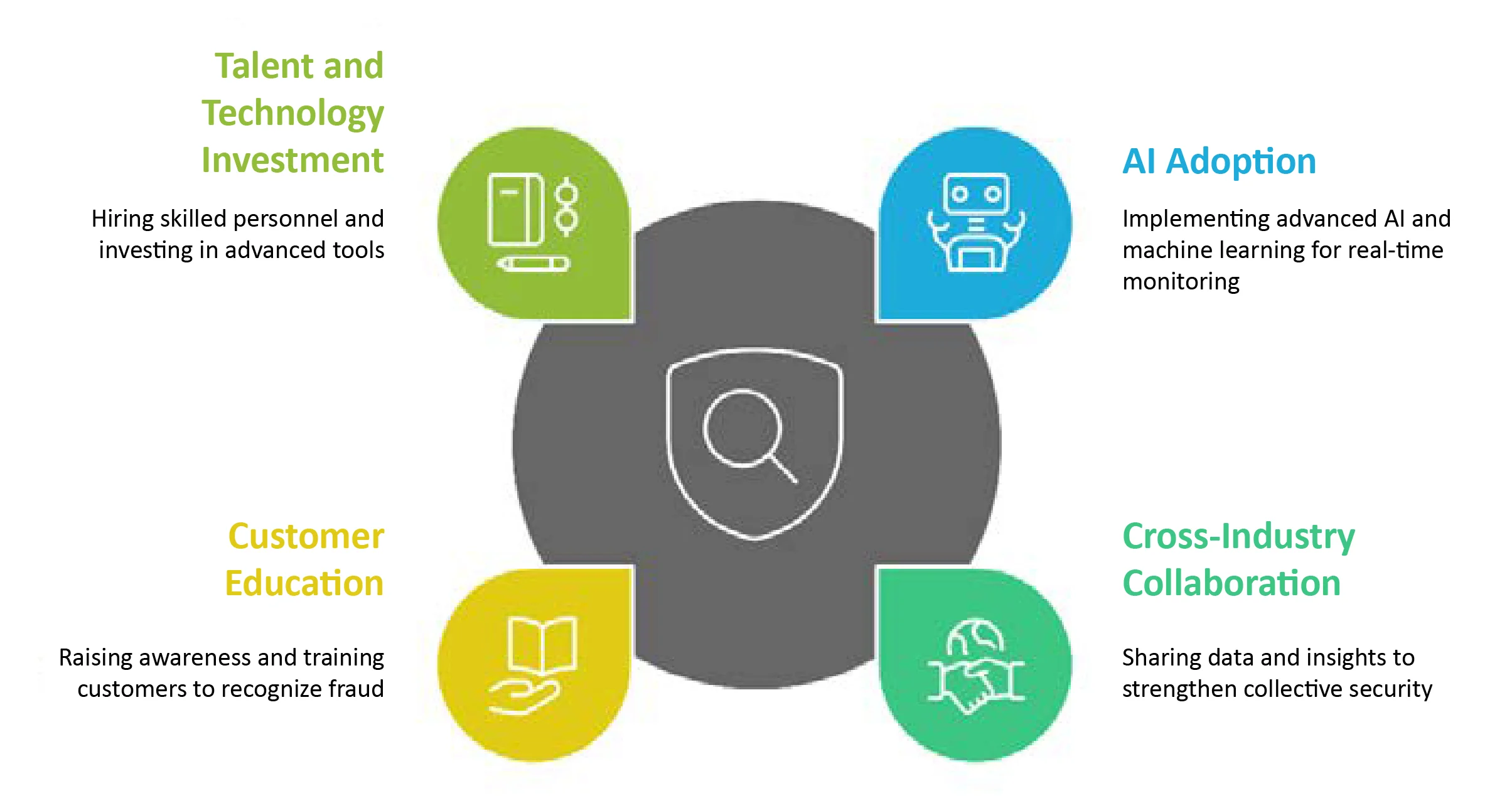

The most obvious answer is to use AI (or better AI) to deal with fraudulent AI. Implementing AI and machine learning solutions can enhance real-time monitoring and detection of fraudulent activities.

To combat such threats, financial institutions must adopt a multi-layered approach. Some examples of successful AI-driven countermeasures solutions:

Liveness detection technology is designed to distinguish between real, live human beings and static images or videos. This technology can detect subtle movements, such as blinking or changes in facial expression, that are difficult for deepfakes to replicate convincingly.

Financial institutions can benefit from sharing data and insights to create a more robust defense against fraud. Collaborative efforts can help standardize data-sharing protocols and enhance collective security measures across the industry.

Building awareness among customers about potential fraud risks is crucial. Financial institutions should provide regular updates and training to help customers recognize and report suspicious activities.

a. Bank of America:

b. Troy Bank & Trust:

Hiring skilled personnel and investing in advanced fraud detection technologies are essential for staying ahead of fraudsters. Continuous training and development of internal teams can foster a culture of vigilance and adaptability.

Source: This article was originally published in “Intelligent Risk by PRMIA” on February, 2025